Budget Model and System

The Office of Budget and Planning (OBP) plays a central role in developing the detailed budget for the Ann Arbor campus. OBP applies the University of Michigan Budget Model (UB Model) and discretionary budget system decisions as it works with schools, colleges and other Ann Arbor campus academic and institutional units to formulate their budgets.

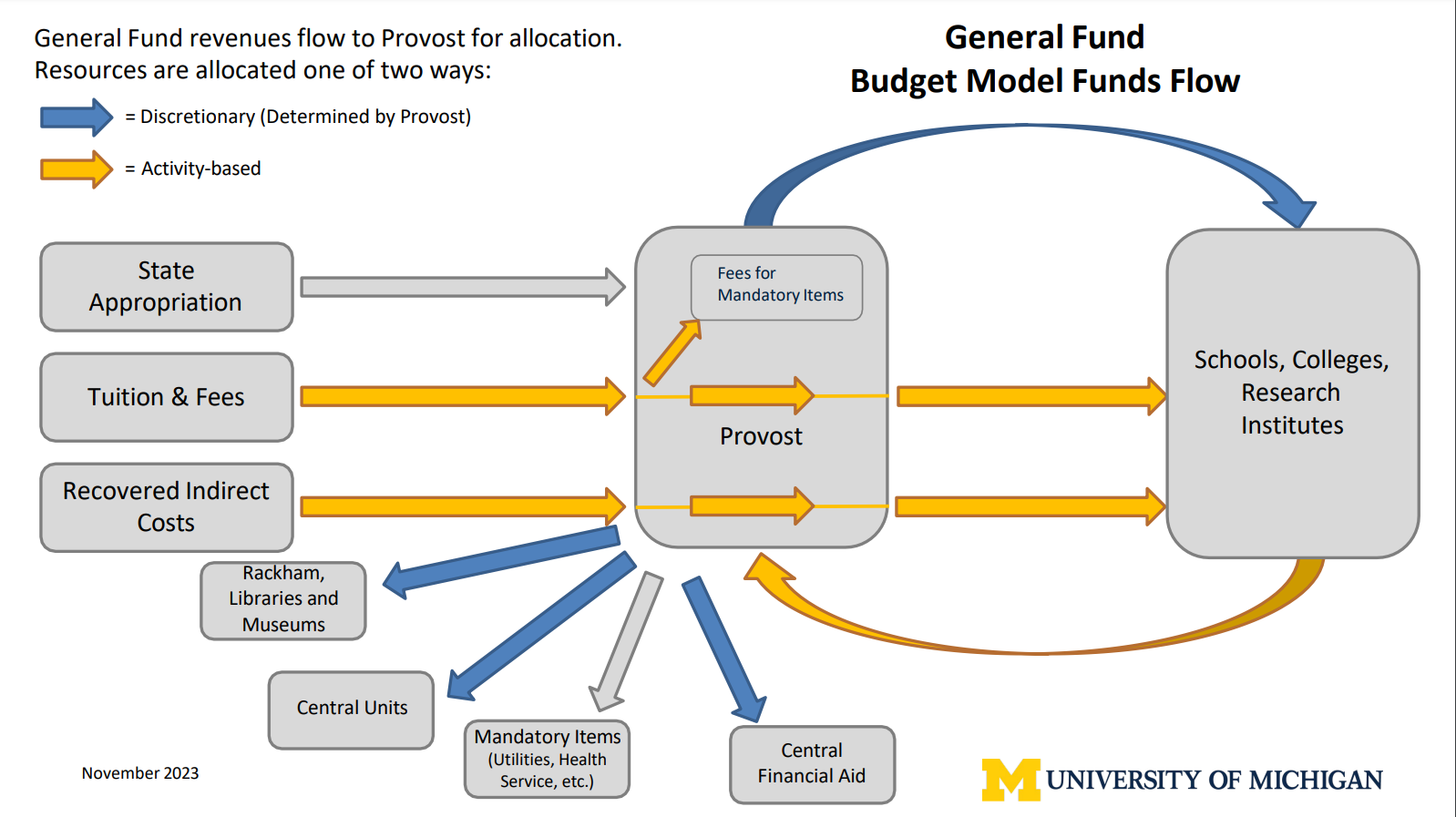

The U-M budget model functions within a hybrid system of responsibility center budgeting, incremental budgeting, and centralized/initiative budgeting. This mix of budgeting allows the University’s leadership to see clearly the fiscal implications of the activities at the school/college/research unit level, while allowing considerable flexibility to set priorities and adjust to fiscal circumstances in light of the University’s missions.

The UB model attributes revenues related to tuition, student fees, indirect cost recovery, and interest; and costs related to financial aid, facilities, and internal assessments to each activity-based unit based on a set of defined rules.

Examples of rules defined in the UB Model:

- Tuition flows to the schools and colleges according to each student’s academic program home unit, as well as student instructional activity of a unit.

- Indirect Cost Recovery (ICR) is generally allocated as revenue to the unit(s) responsible for the direct research associated with the ICR.

- Units with students in the Rackham Graduate School are assessed for financial aid based on their students who are enrolled in Rackham programs.

The Provost has several sources of allocable revenue — increases in state appropriation, increases in facilities-related charges, other internal assessments, and planned reductions in units’ General Fund budgets. These sources are used to support the general operating program, cover increases in mandatory costs, honor base commitments made in prior years, and provide allocations for new initiatives to both academic and non-academic units. These allocation decisions must incorporate the entire set of University needs and explicitly weigh the trade-offs between academic and support priorities.

Key priorities in allocating new funding from the Provost’s office:

- Aligns with university priorities and/or strategic goals of the unit

- Directly enhances academic excellence and/or student success

- Supports cross-unit collaboration

- Supports compliance, safety and/or risk mitigation

- Can leverage additional resources

- Promotes efficiencies within and between units

The links below provide additional description and details about the

U-M model and the broader budget system.

- Budgeting with the University Budget Model [PDF]

Describes University of Michigan budgeting practices and specifics about the University Budget Model. - Annual Budget Presentations to the Regents (leave OBP website)

- Budget Funds Flow Chart [PDF]

- Budget Model Review [PDF]

Summarizes the review of the University Budget Model undertaken in FY19. - General Fund Budget Study, 2006 [PDF] [Abridged Report]

- Capital Planning Process (leave OBP website)

- Office of Government Relations (leave OBP website)

This office coordinates partnerships with the University, local government, and greater Ann Arbor community organizations.

Looking for a specific report or data type? Try the search field at the upper right above, or send a message to [email protected].